Sometimes a manager or an executive will look to buy out existing owners or take over a new business. In these cases, there may be the question of whether one buys the shares or the business assets outright.

Before we delve into 3 things to help determine which one could be best, let's check out some big picture similarities and key differences between a share sale vs. business sale...

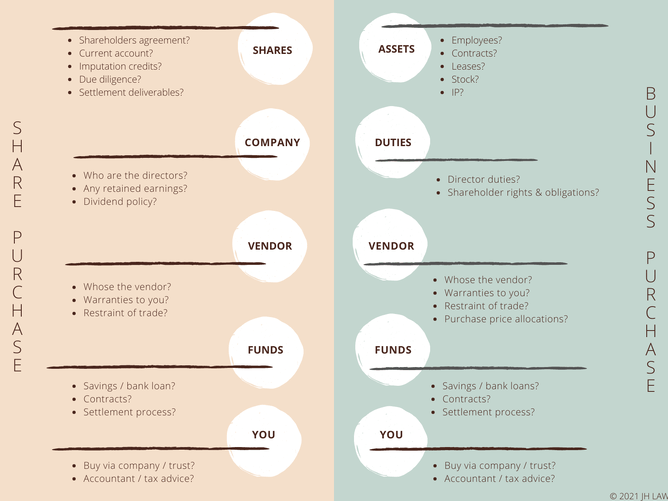

What is the difference between a share sale & business sale?

What is a sale sale? A shareholder decides to sell some or all of their shares, where the sale proceeds go to the shareholder. Once the share sale goes through, the company keeps trading and those shares remain in the company along with all of its existing assets and liabilities.

What is a business sale? The company decides to sell some or all of its assets, where the sale proceeds go to the vendor company. This includes tangible assets (i.e. machinery, equipment), stock in trade and intangible assets (i.e. IP). Where key contracts to leases, suppliers & employees are usually negotiated alongside the asset transfer as well. Once the asset sale goes through, the new owner may keep using the same trading name, but the legal owner will be different and any skeletons from the previous business owner should no longer exist.

1. To decide whether to buy the business or shares, ask yourself how well do you know the business?

I know it very well: If you are well familiar with how the business operates, because you're say already its director or CEO, this may be a classic management buy-out.

You may plan to buy out the existing shareholders. You may already have certain access/authority to deal on behalf of the company/board and have access to its financials and accounts.

Buying the shares means you are taking over the whole history of the business. So if there's going to be a personal grievance, you're probably in the best position to forsee it. If there are tax arrears, again you would likely know. If the company gets slapped with a huge invoice from its supplier that would render it insolvent, you should be able to foresee this (and already have a plan to ensure the company's solvency when that hits).

Yes, there are key warranties and indemnities that you can (and should) put in place to help protect you if nasties appear after you settle the share sale. Although, remember the process to chase and enforce warranties is still one requiring your time and effort where there is no guarantee (unless you specifically ask the vendor to give you one (i.e. personal / bank guarantee)) that the vendor will have the funds to pay you.

I'm not entirely sure: If you've done some due diligence on the business, but still don't feel entirely comfortable with the risk of any skeletons biting you in time, you may be better suited to buy the business assets.

To buy a business means that you'll need to set up new contracts (where relevant) with suppliers, banks, employees and landlords. Note that if these stakeholders don't know you, it may take a while to establish relationships and negotiate trading terms. It's a bit more work, but you keep the nasties away by starting afresh.

2. What are the different contracts and processes involved in a share versus business sale and purchase?

The work required to buy shares versus business assets & contracts can be vastly different.

Due Diligence (both): This step of looking into the business can take a long time. Most of the time, we see clients undergo due diligence before they sign up to the agreement, subject to a confidentiality agreement (NDA). You can also have the agreement subject to DD and use it as grounds to cancel the agreement if DD doesn't work out.

Financing (both): Depending on your source of funding, there may be considerable time spent to engage a broker/investor, prepare term sheets, meet lending conditions & seek legal/tax/accounting advice.

Consents (varies): Examples of various consents to obtain include landlord consent to assign the lease to the purchaser; bank consent to a change in control or release of security & sometimes industry related consents (i.e. dairy supply).

Legal Paperwork (varies):

- Shares: The paperwork pertains more to just the transaction of transferring shares. So were talking share transfer forms, share certificates, waivers of pre-emptive rights, other ways to confirm legal title to the shares, director resolutions, shareholder resolutions, non-competition deeds & written consents.

- Business: The paperwork here on the other hand typically pertains to both the transaction itself and trading contracts / arrangements with people the business works with after the transfer of assets. We're talking assignment of supplier & customer contracts, assignment of lease, asset (tangible & IP) transfer forms, asset certificates, non-competition deeds, written consents, releases from security holders & transfer of employees.

3. Deciding whether to buy shares versus a business will be influenced by the business' tax position.

Business Assets

The tax result from selling assets depends on what type of asset is sold (i.e. tangible, intangible or stock in trade). Each type of asset will be treated differently for tax purposes where the buyer and seller can choose how much of the purchase price can be allocated to each. This arrangement of purchase price allocation for tax purposes is a kettle of fish for another day, although more details can be found here on IRD's website.

Shares

The tax result from selling shares is somewhat simpler than an asset sale. Where generally a vendor will set a price, then the purchaser will pay that price, and any capital gain (or premium paid by the purchaser) is non-taxable income.

It's more the tax considerations before transferring shares where there's a bit more to it. There are two basic tax concepts to consider when transferring a lot of shares, and that is imputation credits and losses. Note that these tax attributes are not transferred on a business (asset) sale, where they remain with the vendor company.

- Imputation Credits: As you will know, companies pay income tax for money they earn in New Zealand. The IRD gives imputations credits to companies that represent how much tax the company has already paid. These credits can be passed onto shareholders alongside any dividends to reduce the tax payable on dividend income received by shareholders. If there are undeclared imputation credits continuity of at least 66% is required to carry forward imputation credits, meaning that one can only sell up to 34% of shares to a new person. When this happens, we may see that the company declares a dividend to clear out the company's imputation credit account before the share sale.

- Losses: On the other hand, in any particular accounting year a company may make a loss. This is when its expenses are greater than its income. Situations where there may be a loss year include being a start up or going a significant stage of expansion. If there are losses to be carried forward continuity of at least 49% is required to carry forward company losses, meaning one can only sell up to 51% of shares to a new person. When this happens, an option can be to use up those losses on trading profits before the share sale.

Parties to any proposed sale of shares should be aware of any outstanding imputation credits or losses to be carried forward.

Take home messages when deciding whether to buy the business or the shares.

- Watch out for business skeletons, especially if you're buying shares.

- Become familiar with what's involved such as the documents, the stakeholders you'll need to reach out to for things like consents / negotiation & your time needed.

- Engage your lawyer, tax & accountant advisors early in the process to save stress and time.

Please reach out to Janey at janey@jhlaw.nz if you have any questions regarding the above. The above is purely for informational purposes, where JH LAW will need to determine if the above information is applicable or appropriate to your particular situation.